12th accountancy public exam answer key 2022 :- Public Exam 2022 for the 12th Standard Students Starts already and today is the Accountancy Public Exam 2022.There is more than Three Lakh Accountancy Students write the Accountancy Public Exam Today. They are eagerly wants to verity the Public Exam answers as quick as possible. 12th Accountancy Public Exam for Tamil medium and English Medium answer key and model question paper available in this website.To provide Public exam 2022 answerkey we provide a good teacher , we collect original question paper quickly because we have a good teachers team.

12th Accountancy Public Exam

We already published 12th english public exam 2022 answer keys and 12th tamil public exam 2022 answer keys.To day the educational department conduct an another exam 12th chemistry public exam 2022. 12th physics public exam 2022 answer keys available another day.

12th accountancy public exam answer key 2022 PDF Download

1.ஒரு கூட்டாளி ஒவ்வொரு மாத இறுதியிலும் ஒரு குறிப்பிட்ட தொகையை வழக்கமாக எடுத்துக்கொள்ளும் போது அந்த எடுப்புகள் மீது கணக்கிடப்படும் வட்டிக்குரிய மாதங்கள் சராசரியாக :

(அ) 12 மாதங்கள் (ஆ) 5.5 மாதங்கள் (இ) 6.5 மாதங்கள் (ஈ) 6 மாதங்கள்

Answer:- (ஆ) 5.5 மாதங்கள்

1.When a partner withdraws regularly a fixed sum of money at the end of every month, period for which interest is to be calculated on the drawings on an average is

(a) 12 months

(b) 5.5 months

(c) 6.5 months

(d) 6 months

Answer:- (b) 5.5 months

2.ஒரு இனம் மற்றொரு இனத்தோடு பெற்றிருக்கும் தொடர்பினை கணிதவியல்

முறையில் கூறுவது

(அ) மாதிரி

(ஆ) முடிவு

(இ) தீர்மானம்

(ஈ) விகிதம்

Answer:- (ஈ) விகிதம்

2.The mathematical expression that provides a measure of the relationship between two figures is called

(b) Conclusion

(c) Decision

(d) Ratio

(a) Model

Answer:- (d) Ratio

3. வருவாய் மற்றும் செலவினக் கணக்கு தயாரிக்கப்படுவதன் மூலம் கண்டறியப்படுவது

(அ) உபரி அல்லது பற்றாக்குறை (ஆ) லாபம் அல்லது நட்டம் (இ) நிதி நிலை (ஈ) ரொக்கம் மற்றும் வங்கி இருப்பு

Answer:- (அ) உபரி அல்லது பற்றாக்குறை

3.Income and Expenditure Account is prepared to find out :

(a) surplus or deficit (c) financial position

(b) profit or loss (d) cash and bank balance

Answer:- (a) surplus or deficit

4.கூட்டாளி சேர்ப்பு தொடர்பாக பின்வரும் கூற்றுகளில் எது உண்மையானதல்ல ?

(அ) கூட்டாண்மை நிறுவனமானது புதிய ஒப்பந்தத்தின் கீழ் மறு கட்டமைக்கப்படும். (ஆ) பொதுவாக கூட்டாளிகளின் பரஸ்பர உரிமைகள் மாறும்.

(இ) ஏற்கனவே உள்ள ஒப்பந்தமானது முடிவுக்கு கொண்டு வரப்படாது. (ஈ) முந்தைய ஆண்டுகளின் இலாபம் மற்றும் நட்டங்கள் பழைய கூட்டாளிகளுக்கு பகிர்ந்தளிக்கப்பட வேண்டும்.

Answer:- (இ) ஏற்கனவே உள்ள ஒப்பந்தமானது முடிவுக்கு கொண்டு வரப்படாது.

4.Which of the following statements is not true in relation to admission of a partner

(a) The firm is reconstituted under a new agreement (b) Generally mutual rights of the partners change

(c)The existing agreement does not come to an end

(d) The profits and losses of the previous years are distributed to the old partner

Answer:- (c)The existing agreement does not come to an end

5.பயனரின் தேவைக்கேற்ப தயாரிக்கப்படும் கணக்கியல் அறிக்கையானது :

(அ) இருப்பாய்வு

(ஆ) வழக்கமான கணக்கியல் அறிக்கை

(இ) இருப்பு நிலைக்குறிப்பு (ஈ) குறிப்பிட்ட நோக்க அறிக்கை

Answer:- (ஈ) குறிப்பிட்ட நோக்க அறிக்கை

5.Accounting report prepared according to the requirements of the user is…..

(a) Trial balance (c) Balance sheet

(b) Routine accounting report (d) Special purpose report

Answer:- (d) Special purpose report

6.பின்வரும் வாக்கியங்களில் எது தவறானது ?

(அ) காப்பு முதல் நிறுமத்தை கலைக்கும் போது செலுத்துமாறு அழைப்பு படுகிறது. விடுக்கப்

(ஆ) வெளியிடப்பட்ட பங்குமுதல் அங்கீகரிக்கப்பட்ட பங்குமுதலை விட ஒருபோதும்

அதிகமாக இருக்கக்கூடாது.

(இ) செலுத்தப்பட்ட பங்குமுதல், அழைக்கப்பட்ட பங்கு முதலின் ஒரு பகுதி ஆகும்.

(ஈ) பங்குகள் குறை ஒப்பமாக இருக்கும் நிலையில் வெளியிடப்பட்ட பங்கு முதல்

ஒப்பிய பங்குமுதலை விட குறைவாக இருக்கும்.

Answer:- (ஈ) பங்குகள் குறை ஒப்பமாக இருக்கும் நிலையில் வெளியிடப்பட்ட பங்கு முதல்

ஒப்பிய பங்குமுதலை விட குறைவாக இருக்கும்.

6.Which of the following statement is false ?

(a) Reserve capital can be called at the time of winding up.

(b) Issued capital can never be more than the authorised capital.

(c) Paid up capital is part of called up capital.

(d) In case of under subscription, issued capital will be less than the subscribed

capital.

Answer:- (d) In case of under subscription, issued capital will be less than the subscribed

capital.

7.நிறுமக் கலைப்பின் போது மட்டுமே அழைக்கப்படக்கூடிய பங்கு முதலின் ஒரு பகுதி

என அழைக்கப்படும்.

(அ) முதலினக் காப்பு (இ) காப்பு முதல்

(ஆ) அங்கீகரிக்கப்பட்ட முதல்

(ஈ) அழைக்கப்பட்ட முதல்

Answer:- (இ) காப்பு முதல்

7.That part of share capital which can be called up only on the winding up of a company is called :

(b) Authorised capital

(a) Capital reserve

(c) Reserve capital

(d) Called up capital

Answer:- (c) Reserve capital

8.நிலை அறிக்கை ஒரு :

(அ) ரொக்க நடவடிக்கைகளின் தொகுப்பு

(ஆ) வருமானம் மற்றும் செலவுகள் அறிக்கை

(இ) கடன் நடவடிக்கைகளின் தொகுப்பு

(ஈ) சொத்துகள் மற்றும் பொறுப்புகள் அறிக்கை

Answer:- (ஈ) சொத்துகள் மற்றும் பொறுப்புகள் அறிக்கை

8.Statement of affairs is a

(a) summary of cash transactions

(b) statement of income and expenditure (c) summary of credit transactions

(d) statement of assets and liabilities

Answer:- (d) statement of assets and liabilities

9.ஒரு குறிப்பிட்ட நோக்கத்திற்காக பெற்ற நன்கொடை :

(அ) வருவாயின செலவு

(ஆ) வருவாயின வரவு

(இ) முதலினச் செலவு

(ஈ) முதலின வரவு

Answer:- (ஈ) முதலின வரவு

9.Donation received for a specific purpose is

(a) Revenue expenditure

(b) Revenue receipt

(c) Capital spenditure

(d) Capital receipt

Answer:- (d) Capital receipt

10.கூட்டாண்மை ஒப்பாவணம் இல்லாத நிலையில் நிறுவனத்தின் இலாபம் கூட்டாளி களிடையே பகிர்ந்தளிக்கப்படுவது :

(அ) சமமான விகிதத்தில்

(ஆ) முதல் விகிதத்தில்

(ஈ) மேற்கூறிய எதுவுமில்லை

(இ) (அ) மற்றும் (ஆ)

Answer:- (அ) சமமான விகிதத்தில்

10.In the absence of a partnership deed, profits of the firm will be

partners in :

(a) Equal ratio

(b) Capital ratio

(d) None of these

(c) Both (a) and (b)

Answer:- (a) Equal ratio

11.பொறுப்புகளைக் காட்டிலும் மிகுதியாக உள்ள சொத்துக்கள்

(அ) முதல்

(ஆ) நட்டம்

(இ) இலாபம்

(ஈ) ரொக்கம்

Answer:- (அ) முதல்

11.The excess of assets over liabilities is

(a) capital

(b) loss

(c) profit

shared by the

(d) cash

Answer:- (a) capital

12.ஒரு நிறுவனத்தின் கடந்த ஐந்து ஆண்டுகளின் இலாபங்கள் பின்வருமாறு : 20144,000; 2015 3,000; 2016 5,000 20174,500 D 2018 3,500.

5 ஆண்டுகளின் சராசரி இலாபம்

(அ) 6,000 (ஆ) T 12,000 () 4,000

(FF) 5,000

Answer:-

12.The following are the profits of a firm in the last five years: 2014: 4,000; 2015: 3,000; 2016: 5,000; 2017: 4,500 and 2018: 3,500. The average profits of five years is

(a) 6,000 (b) 12,000 (c) 4,000

(d) 5,000

Answer:-

13.முகமதிப்பை விட அதிகமாக பெற்ற தொகை வரவு வைக்கப்படும் கணக்கு :

(ஆ) பத்திர முனைமக் கணக்கு

(அ) பங்கு முதல் கணக்கு

(இ) பங்கு ஒறுப்பிழப்புக் கணக்கு (ஈ) அழைப்பு முன்பணக் கணக்கு

Answer:- (ஆ) பத்திர முனைமக் கணக்கு

13.The amount received over and above the par value is credited to

(a) Share capital account (b) Securities premium account

(c)Forfeited shares account (d) Calls in advance account.

Answer:- (b) Securities premium account

14.நிதி நிலை அறிக்கைகள் வெளிக்காட்டாதது

(அ) குறுகிய கால தகவல்கள்

(ஆ) பணம் சாரா தகவல்கள்

(இ) நீண்ட கால தகவல்கள்

(ஈ) கடந்த கால தகவல்கள்

Answer:- (ஆ) பணம் சாரா தகவல்கள்

14.The financial statements do not exhibit :

(a) Short-term data

(b) Non-monetary data

(d) Past data

(c) Long-term data

Answer:- (b) Non-monetary data

15.அறைகலன் கடனுக்கு வாங்கியது Tally-ல் எந்த வகை சான்றாவணத்தில் பதியப்படும் ?

(அ) கொள்முதல் சான்றாவணம்

(ஆ) பெறுதல்கள் சான்றாவணம்

(இ) செலுத்தல்கள் சான்றாவணம்

(ஈ) குறிப்பேடு சான்றாவணம்

Answer:- (ஈ) குறிப்பேடு சான்றாவணம்

15.purchase of furniture is recorded in Tally? In which voucher type credit

(b) Receipt voucher

(d) Journal voucher

(a) Purchase voucher (c) Payment voucher.

Answer:- (d) Journal voucher

16.கீழ்வருவனவற்றில் எது சரியானது?

(அ) உயர் இலாபம் = சராசரி இலாபம் – சாதாரண இலாபம்

(ஆ) உயர் இலாபம் = மொத்த இலாபம்/ஆண்டுகளின் எண்ணிக்கை

(இ) உயர் இலாபம் = சராசரி இலாபம் × கொள்முதல் ஆண்டுகள்

(ஈ) உயர் இலாபம் = கூட்டு இலாபம்/ஆண்டுகளின் எண்ணிக்கை

Answer:- (அ) உயர் இலாபம் = சராசரி இலாபம் – சாதாரண இலாபம்

16.Which of the following is true ?

(a) Super profit= Average profit – Normal profit (b) Super profit=Total profit/number of years

(c) Super profit= Average profit x years of purchase (d) Super profit= Weighted profit/number of years

Answer:- (a) Super profit= Average profit – Normal profit

17.சரக்கிருப்பு மற்றும் முன்கூட்டிச் செலுத்திய செலவுகள் நீங்கலாக உள்ள நடப்புச் சொத்துக்கள் :

(அ) நிதி

(இ) விரைவு சொத்துக்கள்

(ஆ) காப்புகள்

(ஈ) புலனாகும் சொத்து

Answer:- (அ) நிதி

17.Current assets excluding inventory and prepaid expenses is called :

(a) Funds

(b) Reserves.

(c) Quick assets

(d) Tangible assets

Answer:- (a) Funds

18.மறுமதிப்பீட்டு கணக்கு ஒரு………………

(ஆ) சொத்து கணக்கு

(அ) ஆள்சார் கணக்கு

(இ) ஆள்சாரா கணக்கு

(ஈ) பெயரளவு கணக்கு

Answer:- (ஈ) பெயரளவு கணக்கு

18.Revaluation Account is a

(a) Personal Account

(b) Real Account

(c) Impersonal Account

(d) Nominal Account

Answer:- (d) Nominal Account

19.பின்வரும் வாக்கியங்களில் எது சரியானதல்ல ?

(அ) போக்குப் பகுப்பாய்வு என்பது ஓராண்டில் தொகைகளில் ஏற்படும் மாற்றங்களை

ஆய்வு செய்தலைக் குறிப்பதாகும்.

(ஆ) குறிப்புகள் மற்றும் பட்டியல்கள் நிதிநிலை அறிக்கைகளின் பகுதி ஆகின்றன.

(இ) பொது அளவு அறிக்கை சில பொது அடிப்படைகளைக் கொண்டு பல்வேறு இனங்களின் தொடர்பினைக் காட்டுவதாகும். பொது அளவு அடிப்படையின் சதவிகிதமாக காட்டப்படுகின்றன.

(ஈ) நிதி நிலை அறிக்கை பகுப்பாய்வின் கருவிகளில் பொது அளவு அறிக்கை உள்ளடங்கும்.

Answer:- (அ) போக்குப் பகுப்பாய்வு என்பது ஓராண்டில் தொகைகளில் ஏற்படும் மாற்றங்களை

ஆய்வு செய்தலைக் குறிப்பதாகும்.

19.Which of the following statements is not true?

(a) Trend analysis refers to the study of movement of figures for one year.

(b) Notes and schedules also form a part of financial statements.

(c) The common-size statements show the relationship of various items with

some common base, expressed as percentage of the common base.

(d) The tools of financial statement analysis include common-size statement.

Answer:- (a) Trend analysis refers to the study of movement of figures for one year.

20.மறுமதிப்பீட்டின் போது பொறுப்புகளின் அதிகரிப்பு தருவது :

(அ) நட்டம்

(ஆ) இலாபம்

(ஈ) மேற்கண்ட ஏதுமில்லை

(இ) ஆதாயம்

Answer:- (அ) நட்டம்

20.On revaluation, the increase in liabilities leads to :

(a) Loss

(c) Gain

(b) Profit

(d) None of these

Answer:- (a) Loss

பகுதி – II / PART – II

குறிப்பு : எவையேனும் ஏழு வினாக்களுக்கு விடையளிக்கவும். வினா எண் 30-க்கு

கட்டாயமாக விடையளிக்கவும்

Note : Answer any seven questions. Question No. 30 is compulsory.

7×2

நிலை அறிக்கை என்றால் என்ன ?

What is statement of affairs ?

A statement of affairs is a statement showing the balances of assets and liabilities on a particular date. The balance of assets is shown on the right side and the balance of liabilities on the left side. This statement resembles a balance sheet. The difference between the total of assets and the total of liabilities is taken as capital.

Capital = Assets – Liabilities.

உயில் கொடை என்றால் என்ன ?

What is legacy ?

A gift made to a not-for-profit organisation by a will, is called legacy. It is a capital receipt.

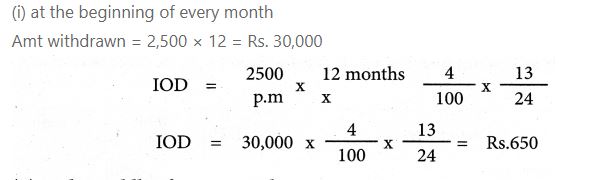

23. கவிதா என்பவர் ஒரு கூட்டாண்மை நிறுவனத்தின் கூட்டாளி. அவர் வழக்கமாக ஒவ் வொரு மாதமும் Rs 2,500 எடுத்துக் கொள்கிறார். எடுப்புகள் மீது வட்டி ஆண்டுக்கு 4% கணக்கிடப்பட வேண்டும். அவர் ஒவ்வொரு மாத தொடக்கத்தில் எடுத்திருந்தால் எடுப்புகள் மீது வட்டி சராசரி கால முறையைப் பயன்படுத்தி கணக்கிடவும்.

23.Kavitha is a partner in a firm. She withdraws Rs. 2,500 p.m. regularly. Interest on drawings is charged 4% p.a., calculate the interest on drawings using average period, if she draws at the beginning of every month.

24.உயர் இலாபம் என்றால் என்ன?

What is super profit ?

Super profit is the excess of average profit over the normal profit of a business.

Super Profit = Average Profit – Normal Profit

25. தியாக விகிதம் என்றால் என்ன ?

25.What is sacrificing ratio ?

The sacrificing ratio is the proportion of the profit which is sacrificed or foregone by the old partners in favour of the new partner. The purpose of finding the sacrificing ratio is to share the goodwill brought in by the new partner.

Sacrifice Ratio = Old share – New share

26.கூட்டாளி விலகல் என்றால் என்ன ?

26.What is meant by retirement of a partner ?

When a partner leaves from partnership firm it is known as retirement. The reasons for the retirement of a partner may be illness, old age, and disagreement with other partners, etc.

27.அப்துல் வரையறு நிறுமம் Rs 10 மதிப்புள்ள 50,000 நேர்மைப் பங்குகளை Rs. 3 முனைமத்தில் வெளியிட்டது. அனைத்து தொகையும் விண்ணப்பத்துடன் செலுத்தப் பட்டது. குறிப்பேட்டு பதிவுகளைத் தரவும்.

27.Abdul Ltd, issues 50,000 equity shares of Rs 10 each payable fully on application. Pass journal entries if shares are issued at a premium of Rs.3 per share.

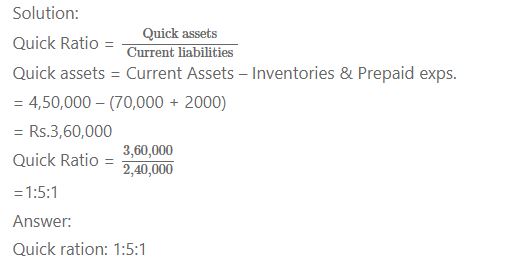

28.கீழ்கண்ட தகவல்களிலிருந்து விரைவு விகிதத்தைக் கணக்கிடவும்.

மொத்த நடப்பு பொறுப்புகள் Rs. 2,40,000; மொத்த நடப்பு சொத்துகள் Rs. 4,50,000; சரக்கிருப்பு Rs 70,000; முன் கூட்டிச் செலுத்திய செலவுகள் Rs. 20,000.

28.Calculate quick ratio from the following details :

Total current liabilities Rs. 2,40,000; Total current assets Rs. 4,50,000; inventories Rs. 70,000; prepaid expenses Rs. 20,000.

29.தானியங்கும் கணக்கியல் முறை என்றால் என்ன ?

29.What is automated accounting system?

Automated accounting is an approach to maintain up-to-date accounting records with the aid of accounting software.

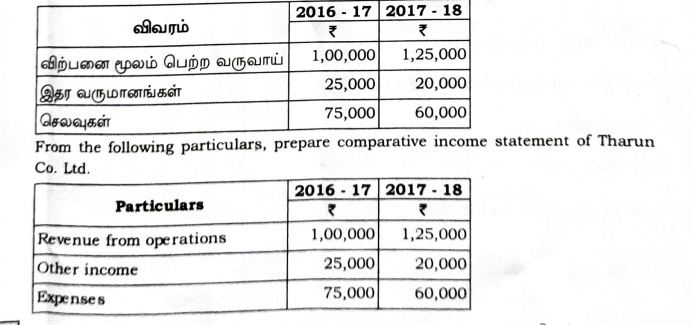

30. பின்வரும் விவரங்களிலிருந்து தருண் கோ நிறுமத்தின் ஒப்பீட்டு வருமான அறிக்கையை தயார் செய்யவும்.

30. From the following particulars, prepare comparative income statement of Tharun Co. Ltd.

பகுதி – III / PART – III

குறிப்பு: எவையேனும் ஏழு வினாக்களுக்கு விடையளிக்கவும். 7×3-2

வினா எண் 40-க்கு கட்டாயமாக விடையளிக்கவும்

Note :Answer any seven questions. Question No. 40 is compulsory.

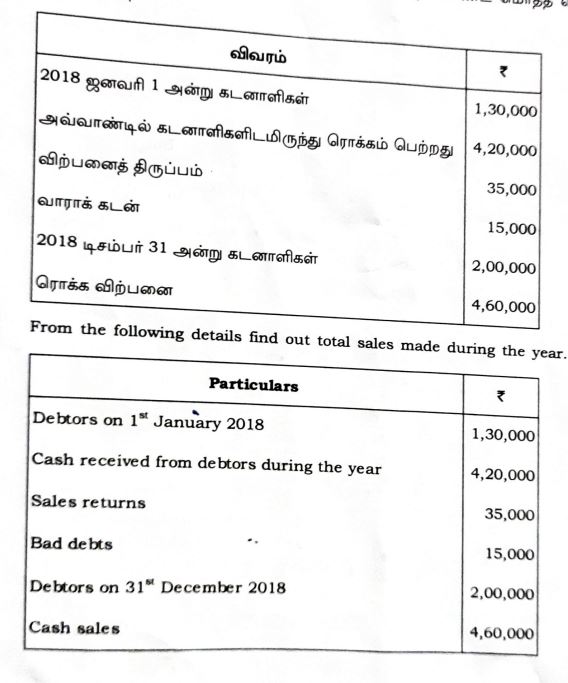

31. பின்வரும் விவரங்களிலிருந்து அவ்வாண்டில் மேற்கொண்ட மொத்த விற்பனையை கண்டறியவும்.

31.From the following details find out total sales made during the year.

9

5957

- ஆகாஷ், பாலா, சந்துரு மற்றும் டேனியல் ஒரு நிறுவனத்தின் கூட்டாளிகள். கூட்டாண்மை ஒப்பாவணம் இல்லாதபோது பின்வருவனவற்றை எவ்வாறு மேற்கொள்வீர்கள் ?

(i) ஆகாஷ் அதிக முதல் வழங்கியுள்ளார். அவர் முதல்மீது வட்டி ஆண்டுக்கு 10% கோருகிறார்.

(ii) ஆகாஷ் இலாபத்தினை முதல் விகிதத்தில் பகிர்ந்தளிக்க வேண்டும் என்கிறார்.

ஆனால் பிற கூட்டாளிகள் அதனை ஒப்புக்கொள்ளவில்லை.

(iii) சந்துருவால் நிறுவனத்திற்கு வழங்கப்பட்ட கடன் ? 50,000. அவர் கடன் மீது

வட்டி ஆண்டுக்கு 12% வேண்டுமென்று கோருகிறார். Akash, Bala, Chandru and Daniel are partners in a firm. There is no partnership deed. How will you deal with the following?

(i) Akash has contributed maximum capital. He demands interest on capital at 10% per annum. (ii) Akash demands the profit to be shared in the capital ratio. But, others do

not agree. (iii) Loan advanced by Chandru to the firm is 50,000. He demands interest on loan @ 12% per annum. - ஒரு நிறுவனத்தின் கடந்த நான்கு ஆண்டுகளின் இலாபங்கள் மற்றும் நட்டங்கள்

பின்வருமாறு :

2015: 15,000; 2016: 17,000; 2017: 6,000 (BLL): 2018: 14,000 4 ஆண்டுகளின் சராசரி இலாபத்தில் 5 ஆண்டுகள் கொள்முதல் என்ற அடிப்படையில் நற்பெயரின் மதிப்பைக் கணக்கிடவும்.

The profits and losses of a firm for the last four years were as follows: 2015 15,000; 2016: 17,000; 2017: 6,000 (Loss); 2018: 14,000 You are required to calculate the amount of goodwill on the basis of 5 years purchase of average profits of the last 4 years. - கூட்டாளி சேர்க்கும் போது மேற்கொள்ள வேண்டிய சரிகட்டுதல்கள் யாவை ? What are the adjustments required at the time of admission of a partner?

- தியாக விகிதத்திற்கும் ஆதாய விகிதத்திற்கும் உள்ள வேறுபாடுகள் யாவை ? Distinguish between sacrificing ratio and gaining ratio.

A

( திருப்புக / Turn over

5957

10

- ராஜன் நிறுமம் 7 6,00,000 மதிப்புள்ள இயந்திரத்தை ஜெகன் நிறுவனத்திடம் இருந்து வாங்கியது. அது பங்கொன்று 7 10 மதிப்புள்ள முற்றிலும் செலுத்தப்பட்ட நேர்மைப் பங்குகளை அவர்களுக்கு செலுத்த வேண்டிய தொகைக்காக வழங்கியது. கீழ்க்கண்ட நிலைகளில் பதிய வேண்டிய குறிப்பேட்டுப் பதிவுகளைத் தரவும்.

(i) பங்குகளை முகமதிப்பில் வெளியிட்டால்

(ii) பங்குகளை 50% முனைமத்தில் வெளியிட்டால் Rajan Ltd. purchased machinery of 7 6,00,000 from Jagan Traders, equity shares of t 10 cach fully paid in satisfaction of their claim. will be made if such issue is made ? It issued What entries

(i) shares issued at par.

at a premium of 50%. - மரியா மற்றும் கலா நிறுமத்தின் பின்வரும் தகவல்களிலிருந்து 2019 மார்ச் 31 -ஆம் நாளோடு முடிவடையும் ஆண்டுக்குரிய பொது அளவு வருமான அறிக்கையைத் தயார் செய்யவும்.

மரியா நிறுமம் |

10,000

கலா நிறுமம்

விவரம்

விற்பனை மூலம் பெற்ற வருவாய்

இதர வருமானம்

செலவுகள்

70,000

30,000

1,20,000

From the following particulars of Maria Ltd. and Kala Ltd., prepare common-size income statement for the year ended 31st March 2019.

Particulars

Maria Ltd.

Kala Ltd.

Revenue from operations

Other income

Expenses

10,000

30,000

70,000

1,20,000

5957

60,000

- பின்வரும் தகவல்களிலிருந்து புற அக பொறுப்புகள் விகிதத்தை கணக்கிடவும்.

11

31.03.2018 அன்றைய இருப்பு நிலைக் குறிப்பு (வருவிய)

விவரம்

I.

பங்கு மூலதனம் மற்றும் பொறுப்புகள் - பங்குதாரர் நிதி

(அ) பங்கு முதல்

நேர்மைப் பங்குகள்

(ஆ) காப்புகள் மற்றும் மிகுதி - நீண்டகாலப் பொறுப்புகள் :

நீண்டகால கடன்கள் (கடனீட்டுப் பத்திரங்கள்)

80,000

3.நடப்புப் பொறுப்புகள் :

(அ) கணக்குகள் மூலம் செலுத்த வேண்டியவைகள்

50,000

(ஆ) இதர நடப்புப் பொறுப்புகள் கொடுபட வேண்டிய செலவுகள்

30,000 3,20,000

மொத்தம்

From the following information calculate debt equity ratio.

Balance Sheet (Extract) as on 31.03.2018

I. Equity and Liabilities

Particulars - Shareholder’s Funds

(a) Share capital

Equity share capital

(b) Reserves and surplus - Non-Current liabilities : Long-term borrowings (Debentures)

- Current liabilities:

(a) Trade payables

(b) Other current liabilities Outstanding expenses

Total

60,000

80,000

50,000

30,000

3,20,000

A

(திருப்புக / Turn over

5957

12

- கணக்கியல் சான்றாவணம் குறித்து சிறு குறிப்பு வரைக. Write a brief note on Accounting Vouchers.

- பின்வரும் விவரங்கள் மார்த்தாண்டம் பெண்கள் பண்பாட்டு மன்றத்தின் இறுதிக் கை குகளில் எவ்வாறு தோன்றும் எனக் காட்டவும்.

1.4.2018 அன்று விளையாட்டுப் பொருள்கள் இருப்பு

அவ்வாண்டில் வாங்கிய விளையாட்டுப் பொருள்கள்

அவ்வாண்டில் பழைய விளையாட்டுப் பொருள்கள் விற்றது

32,000

1,68,000

1,000

31.3.2019 அன்று விளையாட்டுப் பொருள்கள் இருப்பு How will the following appear in the final accounts of Marthandam Women Cultu Association ?

20.000

Stock of sports materials on 1.4.2018

Sports materials purchased during the year

Sale of old sports materials during the year

Stock of sports materials on 31.3.2019

32,000

: 1,68,000

:

1,000 20,000

பகுதி – IV / PART – IV

குறிப்பு : அனைத்து வினாக்களுக்கும் விடையளிக்கவும். Answer all the questions.

Note : - (அ) பின்வரும் விவரங்களிலிருந்து மொத்தக் கொள்முதலைக் கணக்கிடவும்.

விவரம்

2017 ஏப்ரல் 1 அன்று பற்பல கடனீந்தோர்

75,000

2017 ஏப்ரல் 1 அன்று செலுத்தற்குரிய மாற்றுச்சீட்டு

60,000

|கடனீந்தோருக்கு செலுத்திய ரொக்கம் |செலுத்தற்குரிய மாற்றுச்சீட்டுக்கு செலுத்தியது

3,70,000

கொள்முதல் திருப்பம்

15,000

ரொக்க கொள்முதல்

3,20,000

50,000

| 2018 மார்ச் 31 அன்று கடனீந்தோர்

| 2018 மார்ச் 31 அன்று செலுத்தற்குரிய மாற்றுச்சீட்டு

80,000

A

அல்லது

13

5957

(ஆ) அருணன் நிறுமத்தின் 31.03.2019 -ஆம் நாளைய பின்வரும் இருப்பு நிலைக் குறிப்பிலிருந்து :

புற அக பொறுப்புகள் விகிதம் (ii) உரிமையாளர் விகிதம் மற்றும்

(i)

(iii) முதல் உந்துதிறன் விகிதம் கணக்கிடவும்.

விவரம்

I பங்கு மூலதனம் மற்றும் பொறுப்புகள்

1.பங்குதாரர் நிதி

(அ) பங்கு முதல்

நேர்மைப் பங்கு முதல்

1,50,000

1,50,000

8% முன்னுரிமைப் பங்கு முதல்

(ஆ) காப்புகள் மற்றும் மிகுதி 2. நீண்டகாலப் பொறுப்புகள்

நீண்ட காலக் கடன்கள் (9% கடனீட்டு பத்திரங்கள்)

3.நடப்புப் பொறுப்புகள்

(அ) வங்கியிலிருந்து பெற்ற குறுகிய கால கடன்கள்

(ஆ) கணக்குகள் மூலம் செலுத்த வேண்டியவைகள்

25,000

75,000

II. சொத்துகள்

மொத்தம்

- நீண்டகாலச் சொத்துகள்

நிலைச் சொத்துகள்

2.நடப்புச் சொத்துகள்

(அ) சரக்கிருப்பு

7,50,000

(ஆ) கணக்குகள் மூலம் பெற வேண்டியவைகள் (இ) ரொக்கம் மற்றும் ரொக்கத்திற்கு சமமானவைகள்

1,20,000

27,500

2,500

(ஈ) இதர நடப்பு சொத்துகள் : செலவுகளை முன்கூட்டிச் செலுத்தியது

மொத்தம்

A

( திருப்புக / Turn over

5957

14

(a)

From the following particulars calculate total purchases.

Particulars

₹

Sundry creditors on 1 April, Bills payable on 1st April, 2017

2017

75,000

60,000

Paid cash to creditors

3,70,000

Paid for bills payable

Purchases returns Cash purchases

15,000

3,20,000

Creditors on 31 March, 2018 Bills payable on 31 March, 2018

50,000

80,000

OR

From the following Balance Sheet of Arunan Ltd. as on 31.03.2019.

Calculate

(i) Debt-equity ratio

(ii) Proprietary ratio and (iii) Capital gearing ratio

(b)

1,50,000

Particulars

I.

Equity and Liabilities

1.

Shareholder’s funds

(a) Share capital

Equity share capital

8% preference share capital

(b) Reserves and surplus

- Non-current liabilities

Long-term borrowings (9% Debentures) 3. Current liabilities

(a) Short-term borrowings from banks

(b) Trade payables

Total

II. Assets

1,50,000

25,000

75,000 - Non-current assets

Fixed Assets

7,50,000 - Current assets

Inventories

(a)

(b) Trade receivables

(c) Cash and cash equivalents

1,20,000

27,500

(d) Other current assets Expenses paid in advance

Total

2,500

A

5957

15

- (அ) தமிழ் கல்வியியல் மன்றத்தின் கீழ்க்காணும் தகவல்களிலிருந்து 2019 மார்ச் 31-ஆம் நாளோடு முடிவடையும் ஆண்டுக்குரிய பெறுதல்கள் மற்றும் செலுத்தல்கள் கணக்கினைத் தயார் செய்யவும்.

விவரம்

விவரம்

2,10,000

18,000

கட்டடம் வாங்கியது

6,000 பணியாளர் சம்பளம்

55,000 2,65,000

|தொடக்க ரொக்க இருப்பு (1.4.2018)

வாடகை செலுத்தியது

உதவித் தொகை அளித்தது

நுழைவுக் கட்டணம் பெற்றது

15,200

சந்தா பெற்றது

18,500

அல்லது

(ஆ) ஆகாஷ், முகேஷ் மற்றும் சஞ்சய் என்ற கூட்டாளிகள் 3 : 2 : 1 என்ற விகிதத்தில் இலாபங்கள் மற்றும் நட்டங்களைப் பகிர்ந்து வந்தனர். 2017 மார்ச் 31 அன்று அவர்களுடைய இருப்பு நிலைக் குறிப்பு பின்வருமாறு :

சொத்துகள்

|கட்டடம்

1,10,000

40,000

30,000

வாகனம்

26,000

60,000

30,000

25,000

பொறுப்புகள்

|முதல் கணக்குகள் :

ஆகாஷ்

முகேஷ்

சஞ்சய்

இலாபநட்ட பகிர்வு க/கு

பொதுக் காப்பு

தொழிலாளர் ஈட்டுநிதி

செலுத்தற்குரிய மாற்றுச்சீட்டு

|சரக்கிருப்பு

1,30,000

கடனாளிகள்

12,000

கைரொக்கம்

15,000

24,000

18,000

22,000

2,06,000

2,06,000

பகிர்ந்து தரா இலாபம், பொதுக் காப்பு மற்றும் தொழிலாளர் ஈட்டுநிதி போன்றவற்றை பகிர்ந்தளிப்பதற்கான குறிப்பேட்டு பதிவுகள் தருக: மேலும் கூட்டாளிகளின் முதல் கணக்கை தயாரிக்கவும்.

(திருப்புக / Tum over

A

16

5957

(a) From the following particulars of Tamil Educational Society, prepare Receipts and Payments accounts for the year ended 31st March, 2019.

Particulars

₹

Particulars

Opening cash balance as

on 1.4.2018

2,10,000

18,000

Building purchased

55,000 2,65,000

Rent paid

6,000

Staff salary

Scholarship given

15,200 Subscription received

Entrance fees received

18,500

OR

(b) Akash, Mugesh and Sanjay are partners in a firm sharing profits and losses in the ratio of 3 2 1. Their balance sheet as on 31st March, 2017 is as follows:

Liabilities

₹

Assets

Capital accounts:

Buildings

1,10,000

Akash

40,000

Vehicle

30,000

Mugesh

60,000

Stock in trade

26,000

Sanjay

30,000

1,30,000

Debtors

25,000

Profit and Loss appropriation A/c

12,000

Cash in hand

15,000

General reserve

24,000 18,000

Workmen compensation fund

Bills payable

22,000

2,06,000

2,06,000

Pass journal entry to transfer accumulated profit general reserve and workmen compensation fund and prepare the capital account of the partners.

A

17

5957

- (அ) பின்வரும் விவரங்களில் இருந்து உயர் இலாபத்தில் 3 ஆண்டுகள் கொள்முதல் என்ற அடிப்படையில் நற்பெயரின் மதிப்பை கணக்கிடவும்.

(i) பயன்படுத்தப்பட்ட முதல்

(ii) சாதாரண இலாப விகிதம்

15%

(iii) வியாபாரத்தின் சராசரி இலாபம் :

42,000

அல்லது

(ஆ) ஜாய் நிறுமம் 7 10 மதிப்புள்ள 10,000 நேர்மைப் பங்குகளை விண்ணப்பத்தின் போது 7 5, ஒதுக்கீட்டின் போது 7 3, முதலாம் மற்றும் இறுதி அழைப்பின் போது < 2 செலுத்தும் வகையில் வெளியிடப்பட்டது. 9,000 பங்குகளை வாங்க பொது மக்கள் விண்ணப்பித்துள்ளனர். இயக்குநர்கள் 9,000 பங்குகளையும் ஒதுக்கீடு செய்து அதற்கான தொகையையும் பெற்றுக் கொண்டனர். தேவையான குறிப்பேட்டுப் பதிவுகளை தரவும்.

(a) From the following information, calculate the value of goodwill based on 3 years purchase of super profit.

(i) Capital employed

- 2,00,000

(ii) Normal rate of return

: 15%

(iii) Average profit of the business :

42,000

OR

(b) Joy company issued 10,000 cquity shares at ? 10 per share payable 7 5 on application, t 3 on allotment and ? 2 on first and final call. The public subscribed for 9,000 shares. The directors allotted all the 9,000 shares and duly received the money. Pass the necessary journal entries.

A

(திருப்புக / Turm over

5957

18

- (அ) பின்வரும் மலர் நிறுமத்தின் 2016 மார்ச் 31 மற்றும் 2017 மார்ச் 31 -ஆம் நாளைய ஒப்பீட்டு இருப்பு நிலைக் குறிப்பினைத் தயார் செய்யவும்.

| 2016 மார்ச் 31

2017 மார்ச் 31

விவரம்

50,000 - பங்கு மூலதனம் மற்றும் பொறுப்புகள்

- பங்குதாரர் நிதி

(அ) பங்கு முதல்

2,50,000

50,000

(ஆ) காப்பும் மிகுதியும் - நீண்டகாலப் பொறுப்புகள் நீண்ட காலக் கடன்கள்

30,000

60,000

3.நடப்பு பொறுப்புகள்

கணக்குகள் மூலம்

செலுத்த வேண்டியவைகள்

20,000

60,000

மொத்தம்

4,20,000

II. சொத்துகள் - நீண்டகாலச் சொத்துகள்

(அ) நிலைச் சொத்துகள் (ஆ) நீண்டகால முதலீடுகள்

1,50,000

50,000

75,000

2.நடப்புச் சொத்துகள்

சரக்கிருப்பு

75,000

1,50,000

ரொக்கம் மற்றும் ரொக்கத்திற்கு சமமானவைகள்

75,000

45,000

மொத்தம்

4,20,000

அல்லது

(ஆ) ஊட்டி மனமகிழ் மன்றத்தின் பின்வரும் பெறுதல்கள் மற்றும் செலுத்தல்கள் கணக்கிலிருந்து 2018 மார்ச் 31 -ஆம் நாளோடு முடிவடையும் ஆண்டுக்குரிய வருவாய் மற்றும் செலவினக் கணக்கை தயாரிக்கவும்.

பெறுதல்கள்

செலுத்தல்கள்

தொடக்க இருப்பு :

விளையாட்டுப் பொருள்கள்

கை ரொக்கம்

10,000

வாடகை பெற்றது

10,000

எழுது பொருளுக்காக செலுத்தியது

7,000

முதலீடுகள் விற்றது

8,000 கணிப்பொறி வாங்கியது

25,000

சந்தா பெற்றது

54,000

சம்பளம்

20,000

இறுதி இருப்பு

கை ரொக்கம்

15,000

5,000

வாங்கியது

77,000

77,000

A

5957

19

(a) From the following particulars, prepare comparative balance sheet of Malar Ltd. as on 31st March, 2016 and 31st March, 2017.

31st March, 2016

31st March, 2017

Particulars

I. Equity and Liabilities 1. Shareholder’s fund

2,50,000

(a) Share capital (b) Reserves and surplus

50,000

50,000

- Non-current liabilities

30,000

60,000

Long-term borrowings 3. Current liabilities

60,000

Trade payables

20,000

4,20,000

Total

II. Assets - Non-current assets

1,50,000

50,000

75,000

(a) Fixed assets

(b) Non-current investments - Current assets Inventories

75,000

1,50,000

75,000

45,000

Cash and cash equivalents.

4,20,000

Total

OR

(b)

From the following Receipts and Payment Account of Ooty Recreation Club, prepare income and expenditure account for the year ended 31.03.2018.

₹

Payments

₹

Receipts

To opening balance

Cash in hand

10,000

By sports materials purchased

5,000

7,000

To rent received

25,000

To sale of investments

10,000 By stationery paid.

8,000

By computer purchased

54,000 By salaries

By closing balance

20,000

To subscription received

Cash in hand

15,000

77,000

77,000

( திருப்புக

/ Turn over

A

5957

20

- (அ) ஸ்ரீராம் மற்றும் ராஜ் எனும் கூட்டாளிகள் முறையே 2 : 1 எனும் விகிதத்தில் இலாப நட்டங்களை பகிர்ந்து வந்தனர். 1.4.2017 அன்று நெல்சன் என்பவரை புதிய கூட்டாளியாக சேர்த்தனர். கீழ்க்கண்ட சரிக்கட்டுதல்கள் மேற்கொள்ளப்பட வேண்டும்.

(i) சரக்கிருப்பு மதிப்பை 7 5,000 உயர்த்த வேண்டும்.

(ii) ஏடுகளில் பதிவு பெறாமலுள்ள முதலீடுகள் T 7,000 தற்போது பதிவு செய்தல் வேண்டும்.

(iii) அலுவலக சாதனங்கள் மதிப்பை < 10,000 குறைக்க வேண்டும். (iv) கொடுபடாமலுள்ள கூலி 7 9,500 -க்கு வகை செய்ய வேண்டும்.

குறிப்பேட்டுப் பதிவுகள் தந்து மறுமதிப்பீட்டுக் கணக்கை தயாரிக்கவும்.

அல்லது

(ஆ) பின்வரும் விவரங்களிலிருந்து மொத்த விற்பனையை கணக்கிடவும்.

விவரம்

2018 ஏப்ரல் 1 அன்று கடனாளிகள்

2,50,000

60,000

விவரம்

பெறுதற்குரிய மாற்றுச் சீட்டு

15,000

|மறுக்கப்பட்டது

50,000

2018 ஏப்ரல் 1 அன்று பெறுதற்குரிய கடனாளிகளிடமிருந்து பெற்ற ரொக்கம்

மாற்றுச்சீட்டு

உள் திருப்பம்

7,25,000

2019 மார்ச் 31 அன்று

பெறுதற்குரிய மாற்றுச்சீட்டுக்காக ரொக்கம்

பெற்றது

1,60,000

பெறுதற்குரிய மாற்றுச்சீட்டு 2019 மார்ச் 31 அன்று பற்பல

90,000

வாராக்கடன்

கடனாளிகள்

30,000 ரொக்க விற்பனை

2,40,000 3,15,000

(a)

Sriram and Raj are partners sharing profits and losses in the ratio of 2:1 Nelson joins as a partner on 18t April, 2017. The following adjustments are to be made:

(1) Increase the value of stock by 5,000.

(ii) Bring into record investment of 7,000 which had not been recorded in the books of the firm. (iii) Reduce the value of office equipment by T 10,000.

(iv) A provision would also be made for outstanding wages for 7 9,500.

Give journal entries and prepare revaluation account.

OR

5957

21

(b)

From the following particulars, calculate total sales.

15,000

Particulars

Debtors on 1 April 2018

|Bills receivabe on 1″ April 2018

Cash received from debtors |Cash received for bills receivable

Particulars

2,50,000 Bills receivable

dishonoured 60,000 Returns inward

7,25,000

Bills receivable on 31 March 2019 1,60,000 Sundry de btors on 31″ March 2019

50,000

90,000

2,40,000

Bad debts

3,15,000

30,000 Cash sales

46.

(அ) (i)

கயல், மாலா மற்றும் நீலா என்ற கூட்டாளிகள் தங்கள் இலாபங்களை 2:2:1 என்ற விகிதத்தில் பகிர்ந்து வந்தனர். கயல் என்பவர் கூட்டாண்மையை விட்டு விலகுகிறார். மாலா மற்றும் நீலாவுக்கும் இடையே உள்ள புதிய இலாப பகிர்வு விகிதம் 3 : 2 ஆதாய விகிதத்தை கணக்கிடவும்.

(ii) சுனில், சுமதி மற்றும் சுந்தரி என்ற கூட்டாளிகள் தங்கள் இலாபங்களை 3 : 3 : 4 என்ற விகிதத்தில் பகிர்ந்து வந்தனர். சுந்தரி என்பவர் கூட்டாண்மையை விட்டு விலகுகிறார் மற்றும் அவருடைய பங்கு முழுவதையும் சுனில் எடுத்துக் கொள்கிறார். புதிய இலாப பகிர்வு விகிதம் மற்றும் ஆதாய விகிதத்தைக் கணக்கிடவும்.

அல்லது (ஆ) யாஸ்மின் மற்றும் சக்தி நிறுமத்தின் பின்வரும் தகவல்களிலிருந்து பொதுஅளவு நிதிநிலை அறிக்கையினைத் தயார் செய்யவும்.

| யாஸ்மின் நிறுமம்

சக்தி நிறுமம்

விவரம்

50,000

60,000

1,50,000

1,80,000

60,000

I. பங்கு மூலதனம் மற்றும் பொறுப்புகள்

- பங்குதாரர் நிதி

(அ) பங்கு முதல்

(ஆ) காப்பும் மிகுதியும் - நீண்டகாலப் பொறுப்புகள்

நீண்டகாலக் கடன்கள் 3.நடப்புப் பொறுப்புகள்

கணக்குகள் மூலம் செலுத்த வேண்டியவைகள்

மொத்தம்

II. சொத்துகள் - நீண்டகாலச் சொத்துகள்

(அ) நிலைச் சொத்துகள் (ஆ) நீண்டகால முதலீடுகள் - நடப்புச் சொத்துகள்

சரக்கிருப்பு

ரொக்கம் மற்றும் ரொக்கத்திற்கு சமமானவைகள்

மொத்தம்

50,000

1,20,000

90,000

50,000

90,000

( திருப்புக / Turn over

A

5957

22

(a)

(i) Kayal, Mala and Neela are partners sharing profits in the ratio of 2:21. Kayal retires and the new profit sharing ratio between Mala and Neela is 3: 2. Calculate the gaining ratio.

(ii) Sunil, Sumathi and Sundari are partners sharing profits in the ratio of 3:34. Sundari retires and her share is taken up entirely by Sunil. Calculate the new profit sharing ratio and gaining ratio.

OR

(b) Prepare common-size statement of financial position for the following particulars of Yasmin Ltd. and Sakthi Ltd.

Particulars

I.

Equity and Liabilities

- Shareholder’s fund

Yasmin Ltd.

₹

Sakthi Ltd.

₹

(a) Share capital

(b) Reserves and surplus

50,000

60,000 - Non-current liabilities

Long-term borrowings

1,50,000

1,80,000 - Current liabilities.

Trade payables

Total

60,000

II. Assets - Non-current assets

(a) Fixed assets

(b) Non-current investments.

50,000

1,20,000 - Current assets.

Inventories

Cash and cash equivalents

Total

50,000

90,000

90,000

A

23

5957

- (அ) முகேஷ் நிறுமத்தின் பின்வரும் இலாப நட்ட அறிக்கையிலிருந்து

(i) மொத்த இலாப விகிதம்

(ii) நிகர இலாப விகிதம் கணக்கிடவும் முகேஷ் நிறுமத்தின் இலாபநட்ட அறிக்கை.

விவரம்

தொகை - விற்பனை மூலம் பெற்ற வருவாய்

II. இதர வருமானம்

2,50,000

முதலீடு மூலம் வருவாய்

III. மொத்த வருவாய் (I+II)

20,000

2,70,000

|IV. செலவுகள் :

கொள்முதல் செய்த சரக்குகள்

90,000

சரக்கிருப்பு மாற்றம்

10,000

பணியாளர் நலன்களுக்கான செலவுகள்

15,000

இதர செலவுகள்

55,000

வரி ஒதுக்கு

25,000

மொத்த செலவுகள்

1,95,000

V. அவ்வாண்டிற்கான இலாபம்

75,000

அல்லது

(ஆ) கணினிமயக் கணக்கியல் முறையின் பயன்பாடுகளில் ஏதேனும் ஐந்தினை விளக்கவும்.

A

(திருப்புக / Turm over

5957

24

(a)

From the following statement of profit and loss of Mukesh Ltd. Calculate,

(i) Gross profit ratio (ii) Net profit ratio

Statement of Profit and Loss

Amount

Particulars

I. Revenue from operations

2,50,000

II. Other income:

20,000

2,70,000

Income from investment

III. Total revenues (I + II)

IV. Expenses :

Purchase of stock in trade

90,000

10,000

Charges in inventories

Expenses on Employee benefits Other expenses

15,000

55,000

Provision for Tax

Total Expenses

25,000

V. Profit for the year

1,95,000

75,000

OR

(b) Explain any five applications of computerised accounting systems.

A